As RBI mandates banks to be dark pattern free by July, consumers report 8 different dark patterns on online banking platforms

- ● Drip Pricing, Basket Sneaking and Forced Action most common with over 1 in 2 experiencing them

- ● Biggest ever survey on banking dark patterns receives 161,000 responses from consumers located across 388 districts of India

- ● LocalCircles AI powered dark pattern detection engine validated dark patterns reported by consumers and found most online banking apps to have between 4-7 such patterns

February 24, 2026, New Delhi: The Reserve Bank has issued a draft direction proposing tighter norms on marketing and sale of financial products, and banning their bundling by banks, dark patterns apart from mandating explicit customer consent.

The draft ‘Responsible business conduct amendment directions, 2026,’ mandates that all banks must ensure that they do not have any dark patterns by July 2026. LocalCircles had escalated to RBI the need for banks to resolve their dark patterns in September 2025 followed by a reminder in January 2026.

Dark patterns in banking and financial services, according to the Ministry of Consumer Affairs, are deceptive UI/UX designs that mislead or trick users into actions they did not intend. These patterns can impair consumer autonomy and decision-making, amounting to misleading advertising, unfair trade practices, or violations of consumer rights. Examples of this include making it difficult to cancel a recurring service or enrolling users in unwanted products without clear consent as is being witnessed currently in the case of enrolment in government run health insurance schemes. The Central Consumer Protection Authority (CCPA), the regulator, states that dark patterns have emerged as a new form of mis-selling as they are design interfaces and tactics used to trick users into desired behaviour. “The Central Consumer Protection Authority (CCPA) notified guidelines on prevention and regulation of dark patterns on November 30, 2023, with the objective of identifying and regulating such practices.

When it comes to banking, several pitfalls exist for consumers. For instance, a banking app might advertise a free or low-cost service but then add hidden fees, such as transfer fees, maintenance charges or account inactivity fees when the user initiates a transaction. These fees are revealed only when the user is about to complete the process. The result is unexpected charges or fees appear at the last stage of a transaction after the user has already invested time and effort. In many other cases, charges are not intimated upfront but later added in the bill.

“Closing an account is far more complicated than opening one. Hidden fees surface at the last moment, and opting out of data sharing feels like navigating a maze. These are not glitches or oversights which are carefully crafted dark patterns designed to manipulate digital users' decisions.

As consumers navigate through dark patterns and the responsive regulator RBI tries to get them resolved, LocalCircles has conducted a nationwide survey to find out how much consumers are affected and whether they are more aware of what the dark patterns are. The survey received over 161,000 responses from users of online banking services located in 388 districts of India. 67% respondents were men while 33% respondents were women. 44% of respondents were from tier 1, 30% from tier 2 and 26% respondents were from tier 3, 4 and rural districts.

57% of online banking users surveyed say that they experienced basket sneaking with online banking platforms where during checkout or transaction finalization additional charges are added with their clear consent or without being pre-disclosed

As increasing number of consumers use online banking services, the survey asked, “How often have you experienced with online banking platforms that during checkout or transaction finalization, additional charges (e.g., convenience fees, insurance, alerts, or services) were added without your clear consent or without being pre-disclosed?” Out of 17,991 who responded to the question 27% stated they have “very frequently” experienced during checkout or transaction finalization that additional charges were added without clear consent or without being pre-disclosed; 30% of respondents stated it has happened “sometimes”; 6% of respondents stated “rarely” have they experienced it; 37% of respondents stated they have “never” experienced it. To sum up, 57% of online banking users surveyed say that they experienced basket sneaking with online banking platforms where during checkout or transaction finalization additional charges are added with their clear consent or without being pre-disclosed.

46% of online banking users surveyed say that they experienced nagging with online banking platforms where repeated or persistent prompts urge them to activate additional services despite previously declining them

Online banking users often face the issue of being persistently urged to subscribe to new services or products which don’t come free of charge. The survey asked online banking users, “How often have you experienced repeated or persistent prompts on online banking platforms urging you to activate additional services (e.g., credit cards, insurance, overdraft protection or investment options) despite previously declining them?” The question received 17,837 responses with 29% stating they have experienced persistent prompts or ‘nagging’ “very frequently”; 17% of respondents stated they have “sometimes” faced nagging; 16% of respondents stated they have “rarely” faced it; 29% of respondents stated they have “never” experienced nagging; and 9% of respondents did not give a clear response. To sum up, 46% of online banking users surveyed say that they experienced nagging with online banking platforms where repeated or persistent prompts urge them to activate additional services despite previously declining them.

51% of online banking users surveyed say that they experienced forced action where they were required to sign up for an unrelated service or provide additional personal information to access a feature or complete a transaction that should not have needed it

Many online banking platforms require the clients to take on additional services or furnish personal details, even as the government keeps warning people not to provide extra details online or on the phone. The survey asked online banking users, “How often have you encountered situations on online banking platforms where you were required to sign up for an unrelated service or provide additional personal information (e.g., PAN, phone number, email) to access a feature or complete a transaction that should not have needed it?” The question received 18,626 responses. 14% of respondents stated they have “very frequently” experienced such a situation, also known as Force Action; 37% of respondents stated they have faced it “sometimes”; 8% of respondents stated they have “rarely faced this issue; 38% of respondents stated they have “never” encountered such a situation and 3% of respondents did not give a clear answer. To sum up, 51% of online banking users surveyed say that they experienced forced action where they were required to sign up for an unrelated service or provide additional personal information to access a feature or complete a transaction that should not have needed it.

45% of online banking users surveyed say that they experienced subscription trap where the service could be easily initiated online but required visiting a physical branch or contacting customer support during business hours for cancellation

Often people subscribe for a product or service to try it out but later find it difficult to discontinue it if it is found unsatisfactory or not useful. The survey asked online banking users, “How frequently have you encountered situations on online banking platforms where an account or service functioned as a “subscription trap” – that is, the service could be easily initiated online but required visiting a physical branch or contacting customer support during business hours for cancellation, thereby discouraging users from terminating the service or subscription?” The question received 18,030 responses with 25% stating they have encountered subscription traps “very frequently”; 20% of respondents stated they have “sometimes” encountered them; 20% of respondents stated they have “rarely” encountered them; 31% of respondents stated they have “never” encountered them and 4% of respondents did not give a clear answer. To sum up, 45% of online banking users surveyed say that they experienced subscription trap where the service could be easily initiated online but required visiting a physical branch or contacting customer support during business hours for cancellation.

46% online banking users surveyed say that they experienced bait and switch where the product or service ultimately provided or initiated differed from what was originally presented or agreed to at the time of sign-up

Making an offer through advertisements or online platform that looks attractive and later not delivering on promise or giving something else than what was offered originally is an oft used black pattern. The survey asked online banking users, “How frequently have you experienced a ‘bait and switch’ scenario while using online banking platform – where the product or service ultimately provided or initiated differed from what was originally presented or agreed to at the time of sign-up?” Out of 34,869 who responded to the question 25% stated they have “very frequently” experienced ‘bait and switch’ scenario; 21% of respondents stated they have “sometimes” faced it; 9% of respondents stated they have “rarely” experienced it; 29% of respondents stated they have “never” experienced it and 16% of respondents did not give a clear answer. To sum up, 46% online banking users surveyed say that they experienced bait and switch where the product or service ultimately provided or initiated differed from what was originally presented or agreed to at the time of sign-up.

37% online banking users surveyed say that they experienced interface interference where the interface was altered or redirected to promote or offer an unrelated product or service for purchase

The ease of being able to handle bank accounts online has been attracting an increasing number of customers. However, this benefit seems to come with some disadvantages as the banks tend to use their platform to promote new products and services which may not necessarily be of interest to the customer. The survey asked online banking users, “How frequently have you experienced interruptions while transacting on online banking platforms, where the interface was altered or redirected to promote or offer an unrelated product or service for purchase?” Out of 18,151 who responded to the question 12% stated they have experienced interface interference “very frequently”; 25% of respondents stated they have faced it “sometimes”; 18% of respondents stated they have “rarely” faced this dark pattern; 40% of respondents stated they have “never” experienced it and 5% of respondents did not give a clear answer. To sum up, 37% of online banking users surveyed say that they experienced interface interference where the interface was altered or redirected to promote or offer an unrelated product or service for purchase.

64% online banking users surveyed say that they experienced hidden charges/drip pricing on transactions, which were not transparently disclosed at the time of initiation but were debited from their account subsequently

Hidden or charges without prior information by banks is something many customers face, resulting in the aggrieved customers spending considerable time striving to get it reverted. The survey asked online banking users, “How frequently have you encountered instances where online banking platforms levy hidden charges (excluding statutory taxes) on transactions, which were not transparently disclosed at the time of initiation but were debited from your account subsequently?” Out of 18,047 who responded to the question 22% stated they have “very frequently” encountered such situations; 42% of respondents stated they have “sometimes” encountered it; 30% of respondents stated they have “never” experienced it and 6% of respondents did not give a clear answer. To sum up, 64% of online banking users surveyed say that they experienced hidden charges/drip pricing on transactions, which were not transparently disclosed at the time of initiation but were debited from their account subsequently.

45% of online banking users surveyed say that they experienced trick questioning where they encountered confusing or misleading language while navigating or making selections on online banking platforms - such as opting out of messages or declining offers

Making a proposal hard to understand or keeping some vital information hidden or making it difficult to read are some of the misleading tricks used by some banks when striving to sell some service or products. The survey asked online banking users, “How often have you encountered confusing or misleading language (e.g., double negatives, unclear options) while navigating or making selections on online banking platforms – such as opting out of messages or declining offers?” Out of 18,446 who responded to the question 13% stated they encountered misleading or confusing language “very frequently”; 32% of respondents indicated they have “sometimes” encountered it; 18% of respondents stated they have “rarely” encountered it; 31% of respondents stated they have “never” encountered it and 6% of respondents did not give a clear answer. To sum up, 45% of online banking users surveyed say that they experienced trick questioning where they encountered confusing or misleading language while navigating or making selections on online banking platforms - such as opting out of messages or declining offers.

Dark Patterns observed by consumers on online banking platforms

Based on the observation and experience of online banking users, LocalCircles has received dark pattern related complaints for 16 banks, both in the public and private sector and its AI powered dark pattern detection engine has found that on average most banks use 4-7 dark patterns. The banks for which consumers provided inputs include ICICI Bank, HDFC Bank, Axis Bank, State Bank of India (SBI), Vijaya Bank, Kotak Mahindra Bank, Standard Chartered Bank, HSBC, Punjab National Bank (PNB), Bank of Baroda (BOB), IndusInd Bank, IDFC First Bank, Bank of India (BoI), Yes Bank, Central Bank of India, and Paytm Payments Bank.

As far as dark patterns go, Nagging, Drip Pricing, Forced Action and Bait & Switch are the most commonly deployed dark patterns by banks in India though consumers of some banks also experience subscription trap, basket sneaking, disguised ads, interface interference and trick question. For the benefit of understanding, LocalCircles is sharing some of the examples of dark patterns in online banking below.

Examples of Dark Patterns in Banking

Based on consumers complaints and LocalCircles verification, below is an illustration of how dark patterns are being experienced by consumers when using banking apps and websites.

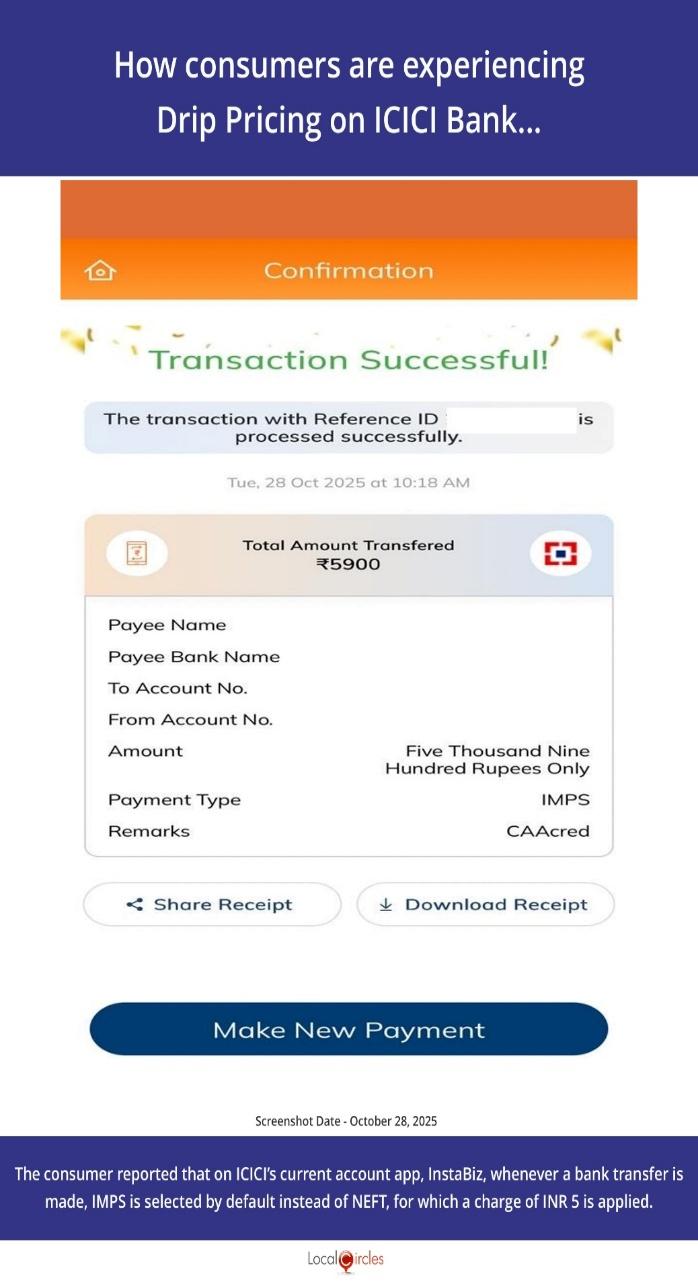

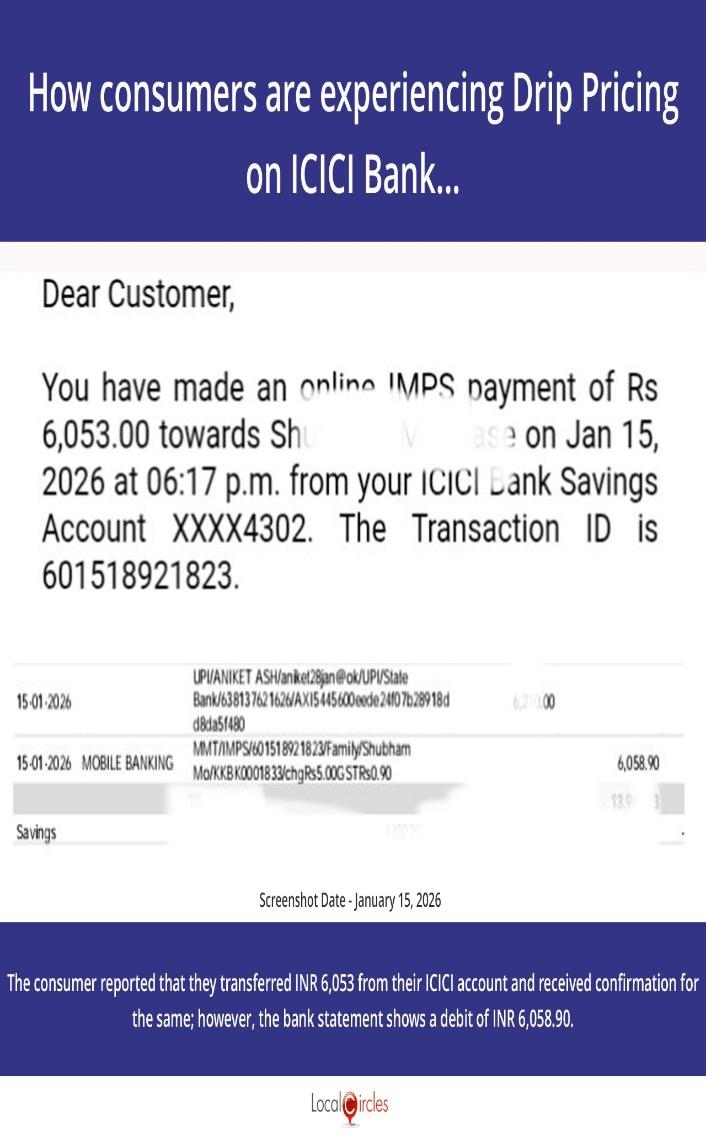

Drip Pricing on online banking platforms involves hiding fees (e.g., convenience, service, or annual charges) that only appear at the final checkout stage. This tactic artificially lowers initial costs, leading users to pay more than expected. It affects 57% of banking consumers as revealed by the LocalCircles survey. The above two screenshots show ICICI Bank consumers experience Drip Pricing dark pattern. (Above left) The consumer reported that on ICICI’s current account app, InstaBiz, whenever a bank transfer is made, IMPS is selected by default instead of NEFT, for which a charge of INR 5 is applied. (Above right) The consumer reported that they transferred INR 6,053 from their ICICI account and received confirmation for the same; However, the bank statement shows a debit of INR 6,058.90.

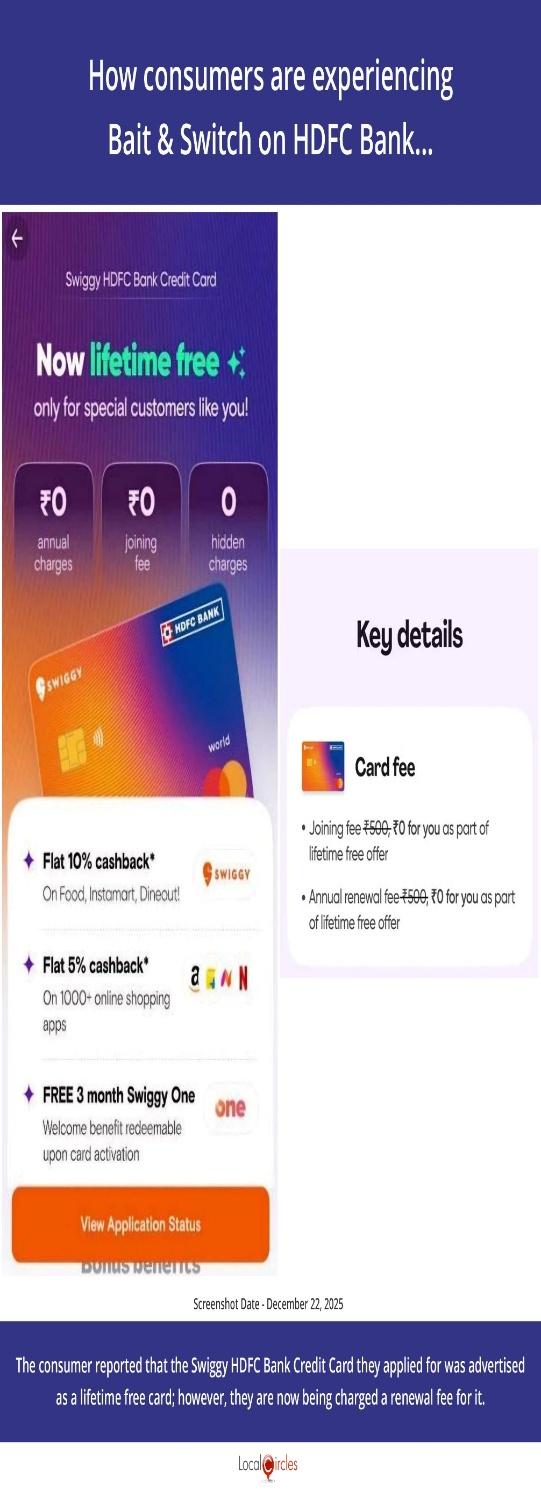

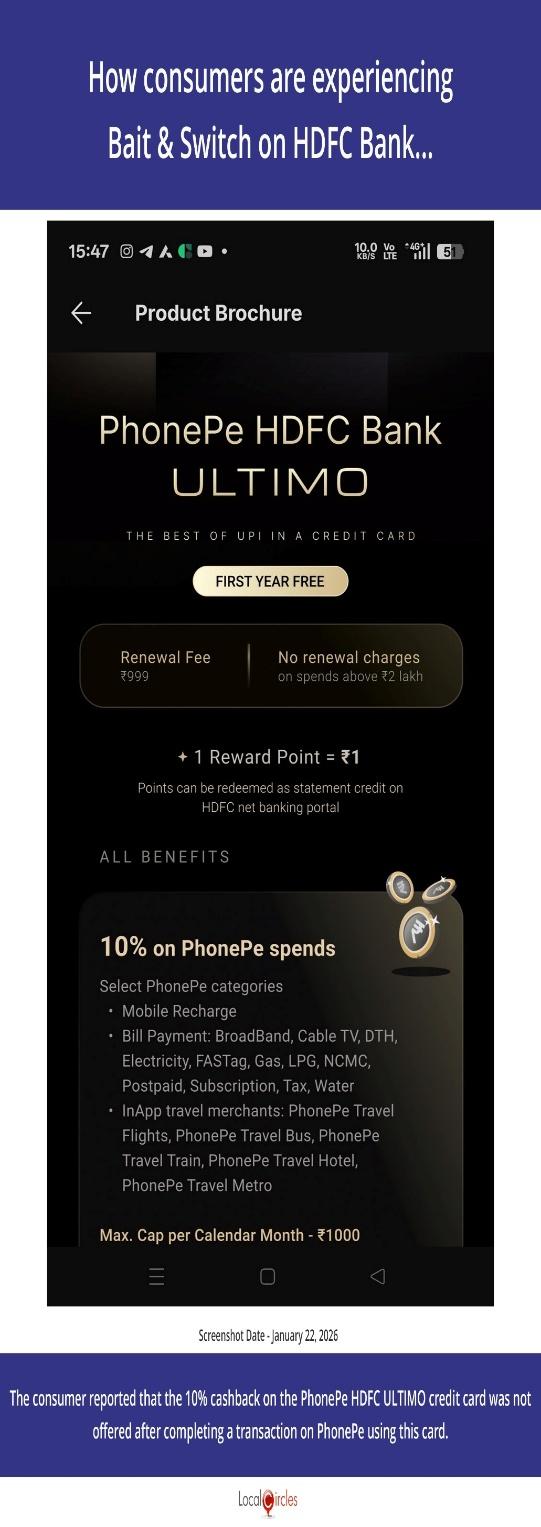

Bait & Switch dark pattern in online banking lures users with favorable, advertised terms—such as zero-fee accounts, high-interest savings, or instant loan approvals—but switches them to inferior, high-cost, or unauthorized products during the digital application process. This deceptive design manipulates users into committing to unfavorable financial services through hidden clauses, complex interfaces, and non-transparent, last-minute changes. Above are two screenshots of how HDFC Bank uses Bait & Switch dark pattern on its online banking platform. (Above left) The consumer reported that the Swiggy HDFC Bank Credit Card they applied for was advertised as a lifetime free card. However, they are not being charge a renewal fee for it. (Above right). The consumer reported that the 10% cashback on the PhonePe HDFC credit card was not offered after completing a transaction on PhonePe using the card.

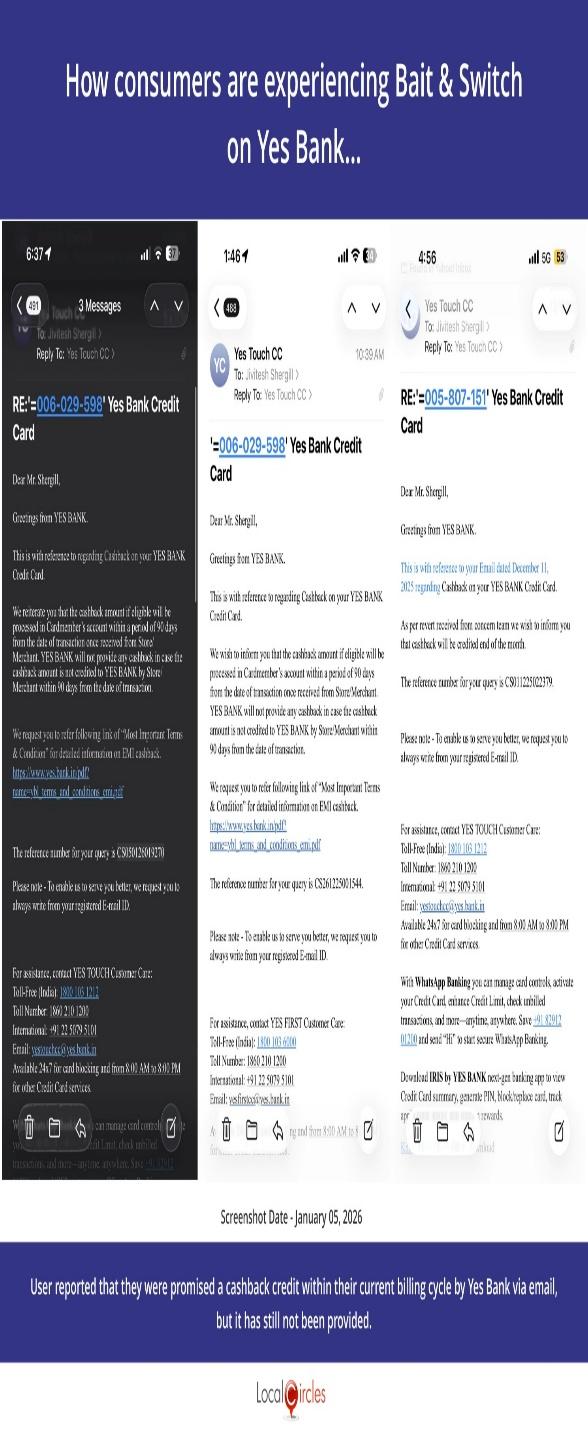

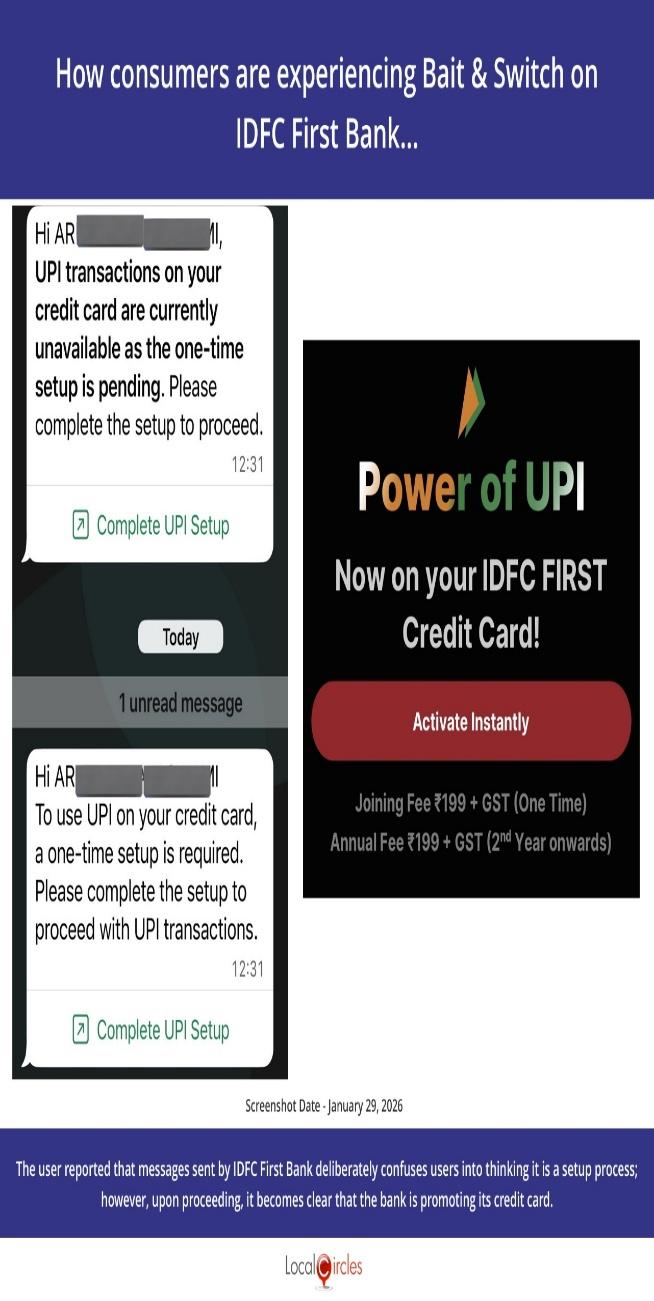

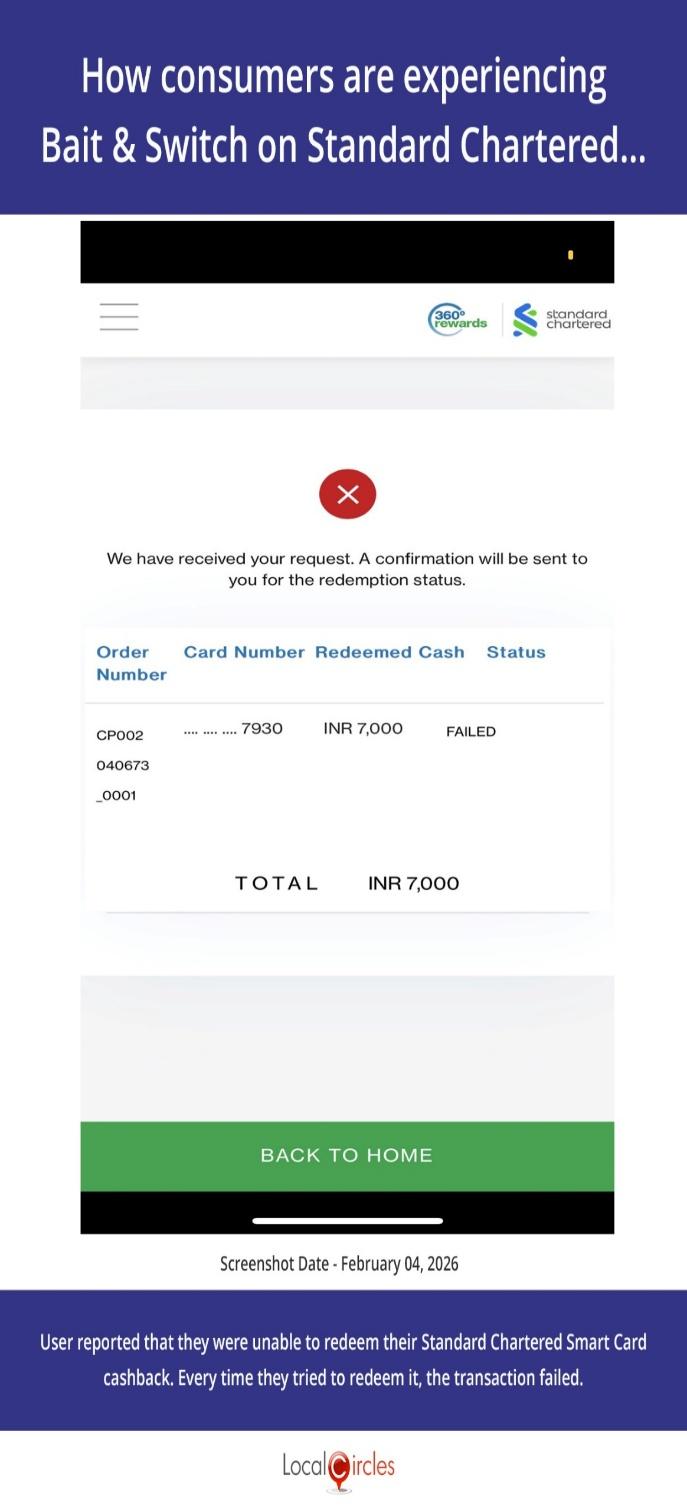

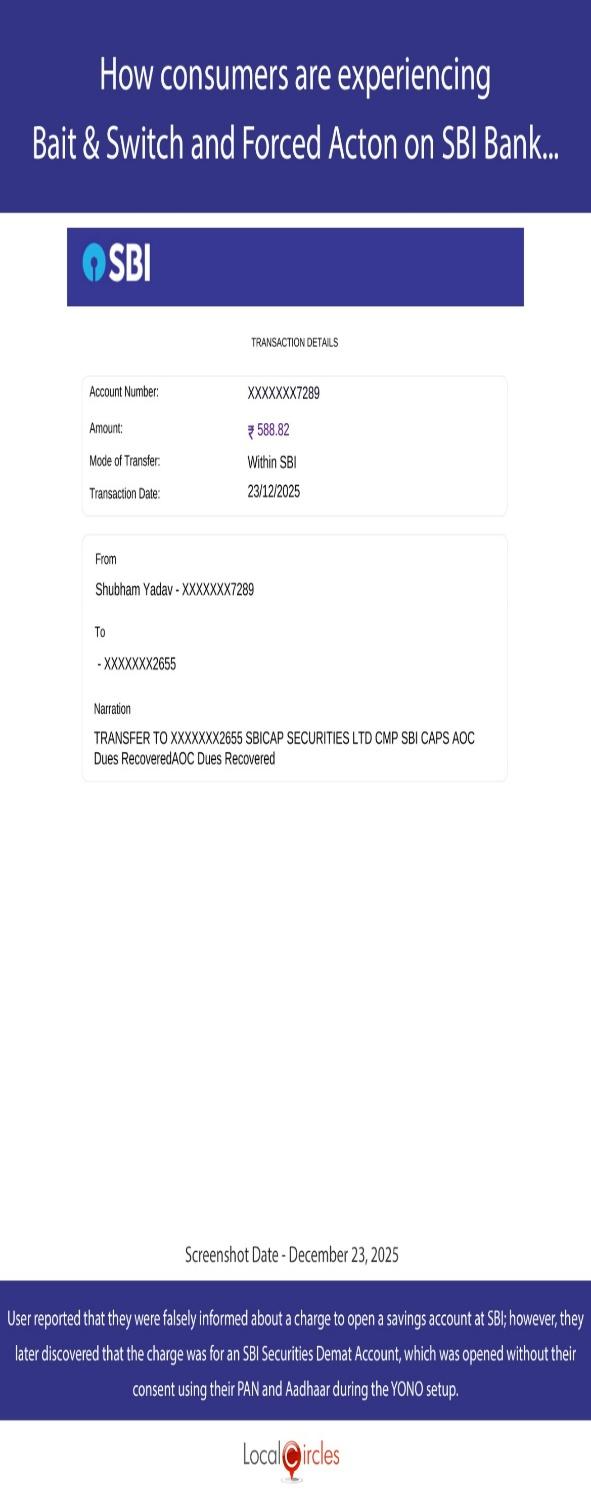

Here are more exampples of Bait & Switch reported by online banking platform users. (Above left) The user reported that they were promised cashback credit within their current billing cycle by Yes Bank via email, but it has still not been provided. (Above right) The user reported that messages sent by IDFC First Bank deliberately confuses users into thinking it is a setup process. However, upon proceeding it becomes clear that the bank is promoting its credit card. (Below left) The user reported that they were unable to redeem their Standard Chartered Smart Card cashback. Every time they tried to redeem it, the transaction failed. (Below right) the user reported that they were falsely informed about a charge to open a savings account at SBI. However, they later discovered that the charge was for a SBI Securities Demat Account, which was opened without their consent using their PAN and Aadhaar cards during the YONO setup.

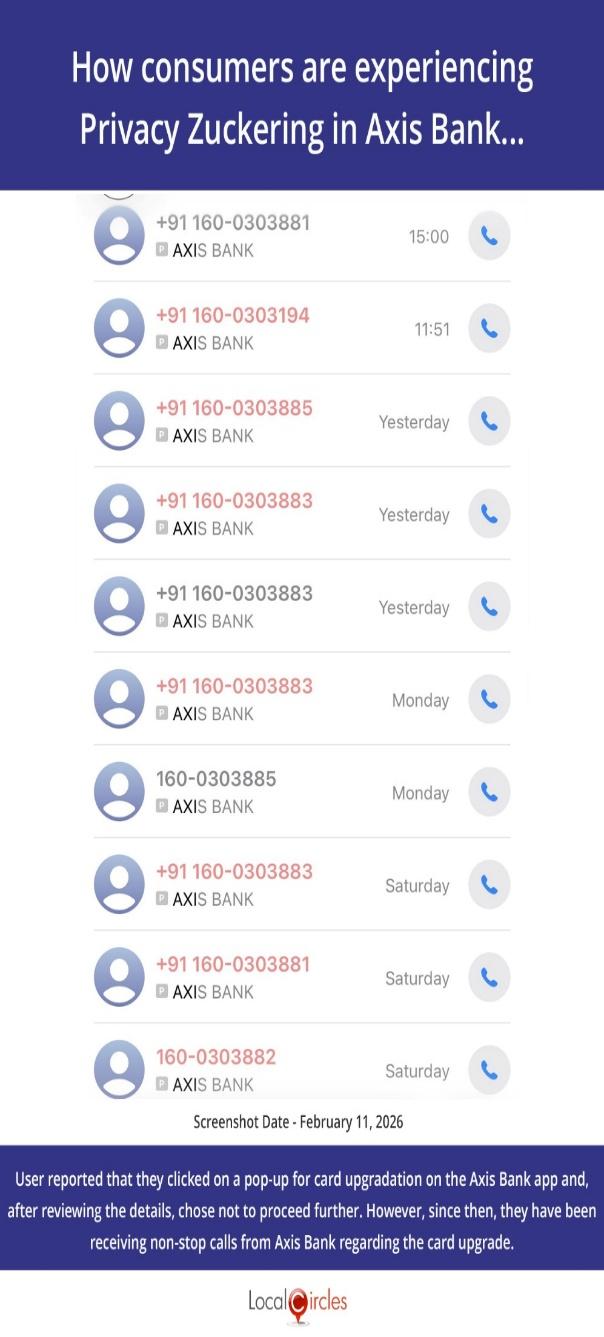

Privacy Zuckering in online banking occurs when platforms use manipulative, complex interfaces to trick users into sharing more personal, financial, or transactional data than intended, often violating the GDPR 'Transparency' principle. The screenshot below (left) shows how consumers are experiencing Privacy Zuckering in Axis Bank. The user reported that they clicked on a pop-up for card upgradation on the Axis Bank app and after reviewing the details chose not to proceed further. However, since then they have been receiving non-stop calls from Axis Bank regarding the card upgrade.

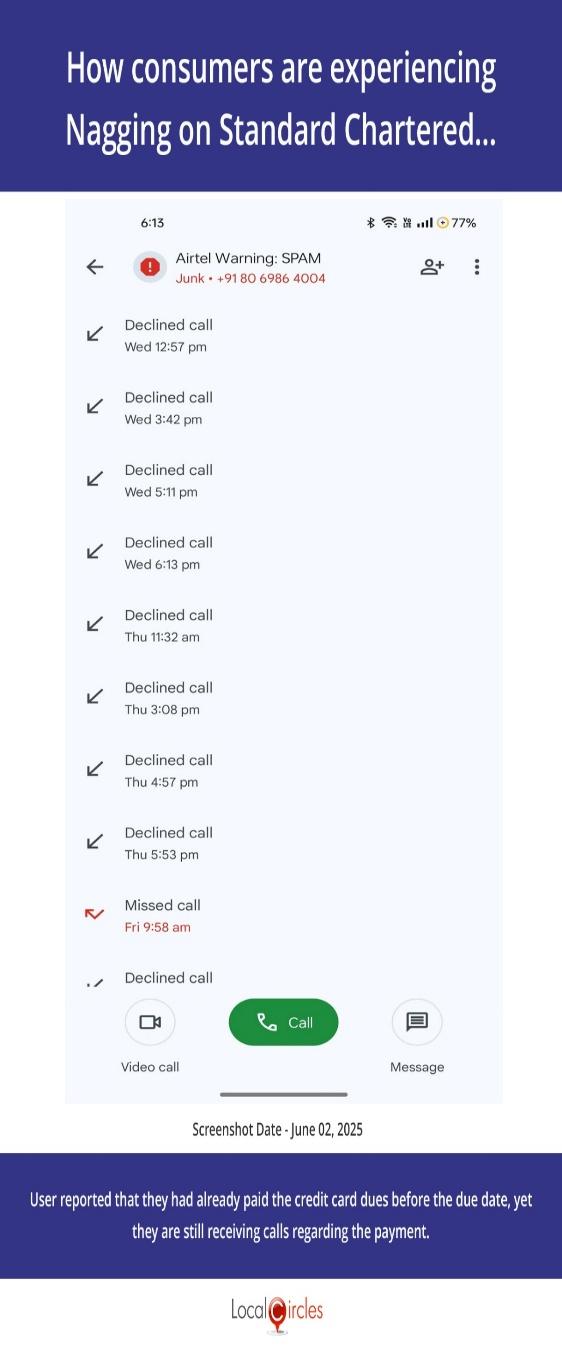

Nagging in online banking involves persistent, disruptive, and annoying prompts—such as constant pop-ups to upgrade, purchase insurance, or enable paperless statements—designed to wear down user resistance and force compliance. Below (right) a Standard Chartered Bank user reported that they had already paid the credit card dues before the due date yet they are still receiving calls regarding the payment.

In summary, the use of some of the dark patterns is very widespread as almost all banks are using them. This is true in the case of Forced Action and Drip Pricing. The study shows that 57% of online banking users surveyed say that they experienced Basket Sneaking with online banking platforms where during checkout or transaction finalization additional charges are added with their clear consent or without being pre-disclosed. 46% of online banking users surveyed say that they experienced nagging where repeated or persistent prompts urged them to activate additional services despite previously declining them. 51% of online banking users surveyed say that they experienced forced action where they were required to sign up for an unrelated service or provide additional personal information to access a feature or complete a transaction that should not have needed it. 45% of online banking users surveyed say that they experienced subscription traps where the service could be easily initiated online but required visiting a physical branch or contacting customer support during business hours for cancellation. 46% online banking users surveyed say that they experienced bait and switch where the product or service ultimately provided or initiated differed from what was originally presented or agreed to at the time of sign-up. 37% of online banking users surveyed say that they experienced interface interference where the interface was altered or redirected to promote or offer an unrelated product or service for purchase. 45% of online banking users surveyed say that they experienced trick questioning where they encountered confusing or misleading language while navigating or making selections on online banking platforms - such as opting out of messages or declining offers. In all the above cases, at least 4 out of 10 users of online banking were impacted. In some cases, the ratio is higher, as in the case of drip pricing. The survey data shows that 64% of online banking users surveyed say that they experienced hidden charges/drip pricing on transactions, which were not transparently disclosed at the time of initiation but were debited from their account subsequently.

The Reserve Bank of India stepping in and mandating the barring of dark pattern usage by banks by July 2026 is a consumer centric move. However, it must be noted that several banks are inefficient, bureaucratic set ups and some are still operating with the same consumer web experience that they had twenty years ago in 2006. Change is hard for banks to implement, harder when it involves technology and business practices. It will take serious checks and balance by RBI not just in July 2026 but every month to ensure there are no surprises in July and every bank is working on resolving these dark patterns.

LocalCircles will escalate the findings of this study to RBI for its awareness and all banks so they can use this as a guide in resolving their dark patterns and become compliant by July 2026.

Survey Demographics

The survey received over 161,000 responses from users of online banking services located in 388 districts of India. 67% respondents were men while 33% respondents were women. 44% of respondents were from tier 1, 30% from tier 2 and 26% respondents were from tier 3, 4 and rural districts. The survey was conducted via LocalCircles platform, and all participants were validated citizens who had to be registered with LocalCircles to participate in this survey.

Survey Methodology

This survey has been conducted using the proprietary LocalCircles stratified sampling methodology. With a minimum target of 30% participation of each gender and a minimum target of 20% participation from each location group (i.e. Metro/Tier 1, Tier 2 & Tier 3-4 & rural) on each poll, all polls were run. After the minimum participation criteria were met, all polls were run till they achieved steady state. Post achievement of steady state, the LocalCircles system using the bootstrapping technique drew additional samples to test for the margin of error. All polls were found to have a margin of error under 3% and a confidence level of over 97%.

About LocalCircles

LocalCircles, India’s leading Community Social Media platform enables citizens and small businesses to escalate issues for policy and enforcement interventions and enables Government to make policies that are citizen and small business centric. LocalCircles is also India’s # 1 pollster on issues of governance, public and consumer interest. More about LocalCircles can be found on https://www.localcircles.com

For more queries - media@localcircles.com, +91-8585909866

All content in this report is a copyright of LocalCircles. Any reproduction or redistribution of the graphics or the data therein requires the LocalCircles logo to be carried along with it. In case any violation is observed LocalCircles reserves the right to take legal action.

Enter your email & mobile number and we will send you the instructions.

Note - The email can sometime gets delivered to the spam folder, so the instruction will be send to your mobile as well